Know your options. Find your path.

If you're thinking about the future — and a move is part of that picture — this is for you.

There's a lot to weigh up. Where you want to be. What you can afford. What matters most at this stage of life. And it can be hard to know where to start.

Here are the most common routes people consider, with a few things worth thinking through for each one — to help you as you're finding the best fit for your situation, not just what's most familiar.

There's no single right answer. What matters is finding what works for you — your situation, your goals, and the kind of life you want in this next chapter.

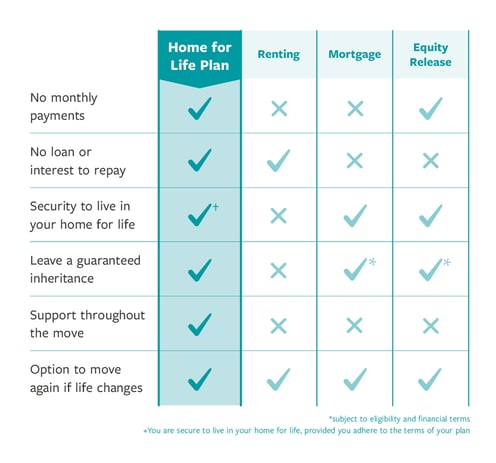

Renting in retirement

Renting can offer real flexibility — particularly if you're not yet sure where you want to live, or you're in a period of change. For short-term situations, it can be a sensible holding position.

If you're thinking about it longer term, it's worth going in with a clear picture of what that looks like in practice. A standard tenancy is typically 12 months. After that, your landlord can ask you to leave and your rent can increase — with limited ability to challenge either. Over time, the costs are ongoing without building any long-term security, and there's nothing to pass on to family further down the line.

None of that means renting is the wrong choice — for some people it's exactly right. But it's worth understanding those realities before committing, so the decision is made with eyes open.

Buying a property outright or with a mortgage

If buying outright is an option — with savings or proceeds from a sale — it gives you full ownership and no ongoing payments to worry about, although your budget may limit the choices of properties you can afford. Plus it's always worth taking independent legal advice and having a clear view of what funds you'd have left over after the purchase to support you in retirement.

If you're considering a mortgage, lenders will assess your age, income, and the term of the loan. Speak to a broker early, as options can be more limited than expected and eligibility criteria vary significantly between lenders.

Monthly repayments are also worth factoring carefully — not just whether they're affordable now, but whether they'd remain comfortable in future years and if circumstances changed. If the numbers work and the terms are clear, it can absolutely be the right route. Going in with a thorough understanding of the commitment is what makes that decision a confident one.

Moving in with family, or accepting their help

For many people, this works beautifully — being close to the people you love, with practical support nearby, can make a real difference to daily life. It's a deeply personal decision, and for some it's exactly the right one.

A few things are worth thinking through before anything is agreed.

-

If you're considering moving into a family member's home: It helps to be clear on who owns the property, what would happen if circumstances changed — if they needed to sell, or if the living arrangement stopped working for everyone — and whether all parties are genuinely aligned on the day-to-day reality.

-

If family are offering financial help: Whether that's contributing to a purchase or sharing ownership, getting the arrangement formalised in writing protects everyone involved. It removes ambiguity and avoids difficult conversations if life takes an unexpected turn.

The more openly these things are talked through at the start, the smoother things tend to be — whatever you decide.

Equity release — if you want to free up money without moving

Equity release is worth a mention here, though it works differently to the other options — it's for people who own a property and want to access funds while staying put. If moving is your goal, it's less likely to be relevant. But if releasing money from your home is part of the picture, it may be worth exploring separately.

The two most common types are:

-

Lifetime mortgage — you borrow against your property and receive a lump sum. Compound interest accrues over time, and the loan is typically repaid from the sale of the property when you pass away or move into permanent care.

-

Home reversion — you sell all or part of your home at below market value in exchange for a lump sum or regular income, and remain in the property.

Both can affect your tax position, benefits entitlement, and what you're able to leave as inheritance. Independent financial advice is an important step before making any decisions here, and it's worth understanding the full long-term picture before committing.

Each of those options has its place. But there's one that often gets overlooked — partly because it works differently to anything else on this list, and partly because not everyone knows it exists...

The Home for Life Plan — a different kind of option

If you're over 60 and thinking about moving, the Home for Life Plan is worth understanding. It's not a mortgage, loan, or equity release. It works differently.

With a Home for Life Plan, you pay a one-off amount — typically a significant saving against the full market price — and secure a Lifetime Lease: the legal right to live in your chosen home for the rest of your life. No rent. No mortgage. No monthly payments. Ever.

The difference comes down to how it's structured. Homewise purchases the property. You purchase the right to live there for life — legally protected, registered with the Land Registry, and yours from day one. And because you're securing a Lifetime Lease rather than buying the property itself, you don't pay the full market price.

When ownership becomes optional, your options open up.

Without a Home for Life Plan, many people find themselves settling for a location that isn't quite right, taking on debt to afford the home they really want, or facing the uncertainty of renting with no long-term security. Feeling like this next chapter isn't starting the way they'd hoped.

With a Home for Life Plan, things can look quite different:

-

Live closer to family, friends, and the people you love

-

Relocate to the coast, countryside, or somewhere more convenient

-

Choose a home that's easier to manage and fits your lifestyle

-

Free up funds to clear outstanding debts or gift an early inheritance

-

Feel settled in the right home, without ongoing financial worry

A few other things worth knowing:

-

Your inheritance choice is yours. You decide what percentage of the property's future value goes to your estate — and it benefits from any rise in property value over time.

-

If life changes, your plan can move with you to another property, subject to the usual checks.

-

You don't go through any of it alone. Homewise's team is with you through the whole process — finding the right home, arranging viewings, managing the sale, liaising with solicitors, and making sure nothing falls through the cracks.

Is it right for everyone? No. But for people who want to move to the home they really want — without the financial pressure of a mortgage or the uncertainty of renting — it can make a real difference.

The most important thing

Whichever route you go with — take your time.

Ask the questions that matter to you. Read the small print. Get independent advice where it's relevant. And make sure you feel genuinely comfortable with what you're agreeing to — not just now, but in the years ahead.

Moving should feel like the start of something. Not a compromise.

Ask us anything, we're here to help.

Our team is happy to talk things through — whether you want to understand your options more clearly, find out if a Home for Life Plan could work for you, or simply see what might be possible. No pressure, no obligation.

Call us free on 0808 303 1683, contact us online or request a copy of our brochure to find out more at your own pace.